Summary

- NVIDIA delivered a strong Q1 2027 driven almost entirely by data centres. Total revenue hit $81.62 billion (up 85% year over year) and free cash flow nearly doubled to a record $48.6 billion. Data centre revenue alone reached $75.25 billion, 92% of total sales, making the company increasingly a single segment story.

- Profitability and margins remain elite, but concentration risk is rising. Gross margin of 75% landed at the top of guidance, EPS of $1.87 beat the $1.76 consensus, and LTM operating margin sits at 60.4%. The flip side: with 92% of revenue from one segment, any slowdown in AI infrastructure spend would hit disproportionately hard.

- Management is openly flagging three structural risks. Hyperscaler customers (Apple, Meta, Microsoft) are building in house AI chips, potentially reducing B2B demand. Access to the Chinese market is at risk as China builds region specific alternatives. And NVIDIA may not recoup investments in new sectors where competitors already have an edge. Jensen Huang himself is acknowledging obsolescence and market share loss as real possibilities, a notable tonal shift from prior quarters.

Thu, May 21

5 min

SGFX research desk

NVIDIA's Q1 2027 earnings exceeds expectations with $81.6 billion in revenue

NVIDIA's Q1 2027 earnings exceeds expectations with $81.6 billion in revenue

Risk Warning: The information in this article is provided for general informational and educational purposes only. It does not constitute investment advice, a personal recommendation, an offer, or a solicitation to buy or sell any security, financial instrument, or product. Investing in equities, indices, ETFs, and other financial instruments involves a significant risk of loss and is not suitable for every investor. Past performance is not a reliable indicator of future results.

Macroeconomic headwinds affecting stocks appear to be on pause temporarily. NVIDIA’s Q1 2027 earnings report showed robust growth, particularly in its data center segment.

- Data Center Revenue reached $75.25 billion, surging 92% year-over-year and now representing 92% of total sales.

- Total Revenue climbed to $81.62 billion, marking an 85% jump compared to the same period last year.

- Free Cash Flow hit a record of $48.6 billion, nearly doubled from $26.1 billion in the prior year.

- Gross Margin came in at 75.0% on a non-GAAP basis, landing at the top end of guidance.

- Adjusted EPS of $1.87 surpassed the consensus analyst's estimate of $1.76.

NVIDIA’s earnings report was not the only reason for increased optimism in stock markets, particularly the technology sector. The market is now feeding a slew of good news, some of which come from the tech sector. Samsung successfully managed to avert a strike which was expected to seriously disrupt operations after which it went up by more than 8%. The strike was averted by giving a lucrative compensation deal to employees specifically based in the semi-conductor division of the company.

However, NVIDIA acknowledges that multiple risks could hamper its business model, most of which come from its occupying a pivotal role in the semiconductor industry. Many of these risks have been acknowledged in a 10-Q filing and they include the following:

- Risk of losing business due to self-sufficiency in production of ASIC and semiconductor products: Multiple reports have been coming in over the last few weeks, and they all point to a clear trend—companies such as Apple, Meta, and Microsoft are actively working to build technologies which cater to their own demand for AI chips and products. Some of these products have to be sourced on a B2B level from NVIDIA simply because they have the capabilities to produce chips of varying sizes and features.

- Losing access to the Chinese market: NVIDIA’s CEO Jensen Huang has already acknowledged this possibility. China’s self-sufficiency in semiconductor materials and tech-focused manufacturing means work is already underway to create a region-specific version of all the products America’s Silicon Valley tech companies are producing.

- Failed investments in new sectors due to competition from other companies: NVIDIA has acknowledged it may not be able to recoup investments targeting growth in sectors where other companies also have a competitive advantage.

The company’s gross margins for the quarter remained healthy at 75% consistent with the LTM rolling average. (Source: TIKR)

- LTM gross margin: 71.1%

- LTM operating margin: 60.4%

- LTM P/E ratio: 45.61x

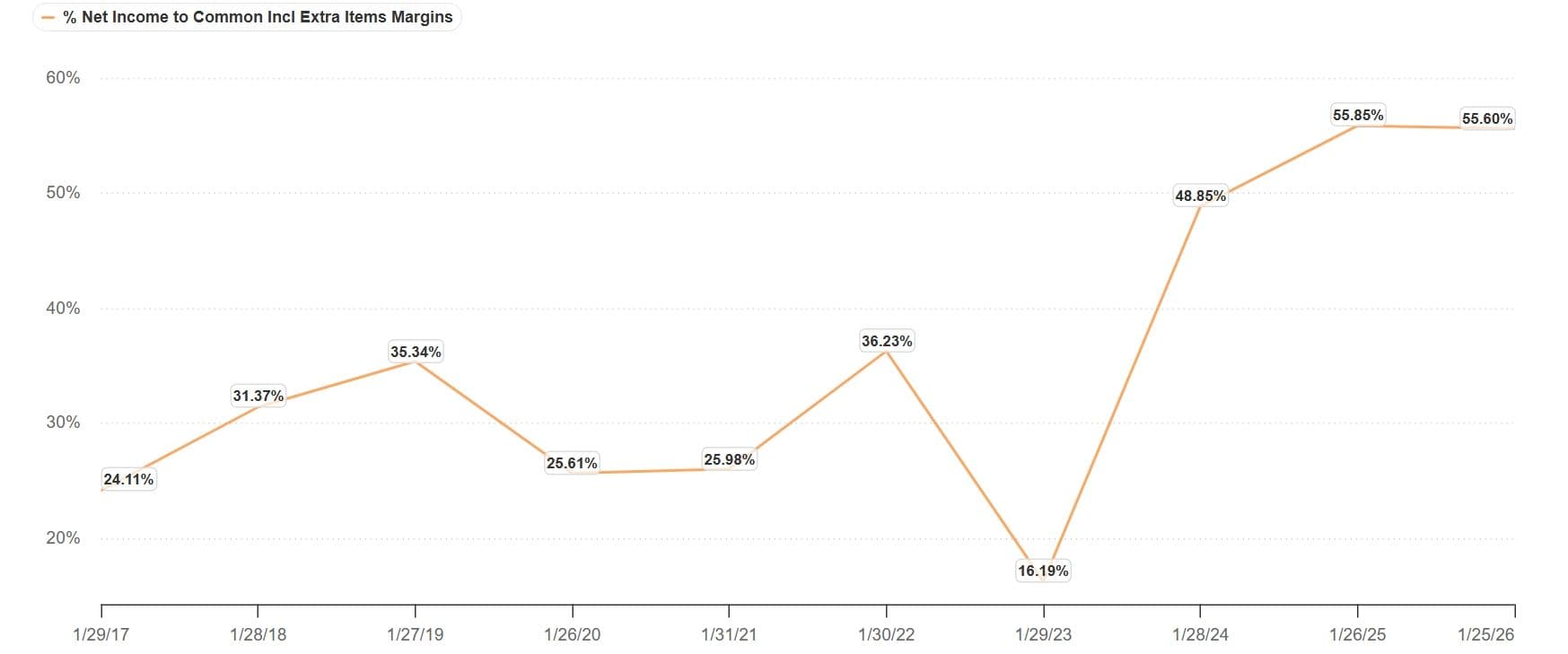

Over the last 9 years, the company’s net margins have also improved, indicating increased profitability.

The forecasted P/E ratio for the next twelve months according to TIKR was fixed at 26.68x. For context, reported P/E averages across related sectors are as follows: — Semiconductor industry: 43x to 51x (Source: full ratio) — Semiconductors and equipment: 58.1x to 60.3x (Source: full ratio) — Nasdaq 100 (QQQ): 26.2x to 27.0x on a forward basis (Source: WorldPEratio)"

NVIDIA’s technology for chips and wide range of products means its rack-scale architecture is used for virtually all companies in the magnificent seven that have investments in data center infrastructure and want to do something for AI.

The applications for NVIDIA’s products still remain far and wide, extending into multiple industries such as healthcare, automobiles, architecture, and others.

Summary

NVIDIA’s revenue growth from catering to firms operating data center infrastructure remains immense. With rapid growth comes new challenges and Jensen Huang and NVIDIA are now fully acknowledging that obsolescence and loss of market share remain a possibility due to the rapid growth of the AI sector worldwide. There are multiple forms of risk now attached to NVIDIA’s business model.

In line with the company’s new resolution to start providing a detailed breakdown of revenue in the data center segment, earnings figure will now be classified into different categories, mainly including its hyperscale clients and customers in government sector and other industries.

Research references

- Nvidia (NVDA) Falls on Disappointing Forecast as AI Chip Competition Mounts - Bloomberg

- TIKR data

- Bloomberg data

- Fullratio.com

- WorldPEratio data

- https://www.cnbc.com/2026/05/21/nvidia-jensen-huang-china-ai-chip-market-huawei.html

- https://www.cnbc.com/2026/05/20/were-raising-our-price-target-on-nvidia-after-another-knockout-quarter-and-guide-.html

- https://www.cnbc.com/2026/05/21/softbank-asia-tech-stocks-nvidia-earnings.html

Disclaimer: This article reflects the views and analysis of the author at the time of publication and is based on information believed to be reliable from publicly available sources. Spectra Global makes no representation or warranty, express or implied, as to the accuracy, completeness, or timeliness of the information contained herein, and accepts no liability for any loss arising from reliance on it. Spectra Global is licensed by the UAE Securities and Commodities Authority (SCA) under Category 5 (Promotion). Nothing in this article should be construed as a personal recommendation or as an inducement to enter into any transaction. Past performance is not indicative of future results.

Stay Ahead of the Market

Subscribe for the Latest Trading News

Get expert insights, market news, and updates straight to your inbox.